Plain-language financial writing since 2012

Keep calm. Stay invested. Build lasting wealth.

Independent financial writing for high-earning professionals navigating RSUs, taxes, markets, and the noise in between. Written by Nirav Desai, founder of Qubera Wealth Management.

Book a Free Consultation →As I mentioned in my previous post, April saw record levels of volatility in the stock market.

The severe market swings weren’t just a knee-jerk reaction to tariffs, but rather a reaction to major shifts in the global economic landscape.

The global economic landscape is changing in significant ways that require thoughtful adjustments to your investment strategy. Recent trade policies are creating ripple effects throughout the global economy that will impact long-term investment returns.

Key Developments Affecting Your Investments

Shifting International Relationships

The current tariff policies are straining relationships with key allies. These actions, intended to bolster domestic industries, are inadvertently pushing some of our closest partners towards nations that are traditionally considered U.S. competitors. This realignment extends far beyond simple trade balances and affects global capital flows.

America’s Changing Economic Position

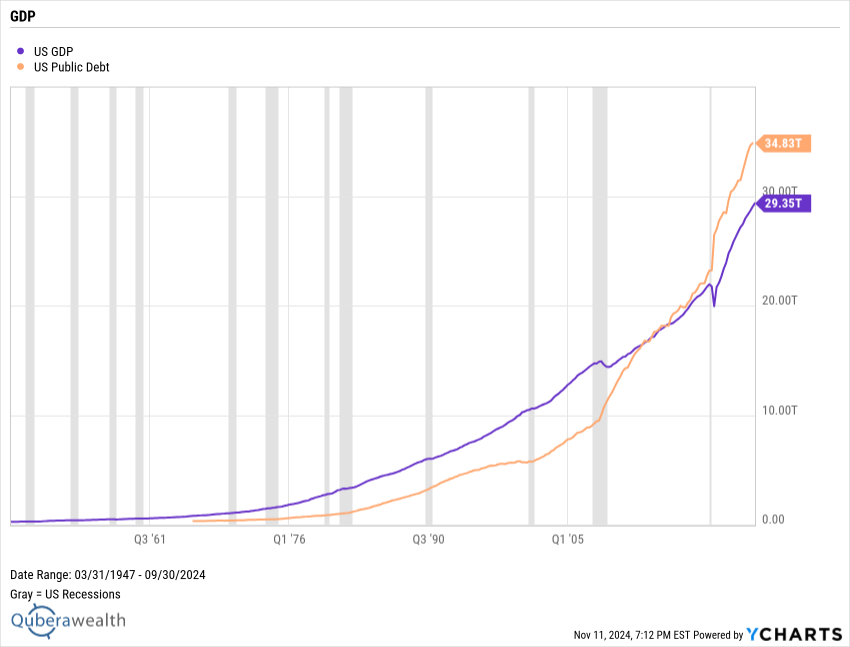

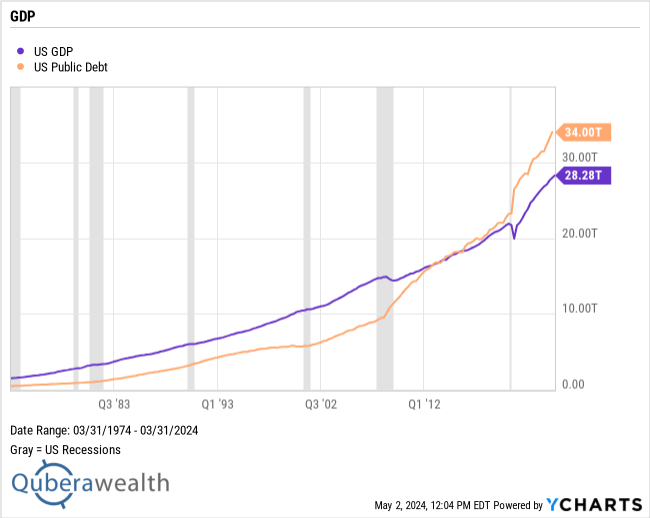

For decades, the U.S. dollar’s status as the world’s primary reserve currency has provided our economy with significant advantages, including lower borrowing costs.

The trade deficit with our trading partners resulted in their accumulating a surplus of U.S. Dollars. These U.S. Dollars were used to buy down U.S. Treasury bonds, pushing down borrowing costs for not only the U.S. Government but also for U.S. home owners, as our mortgage rates are tightly correlated to the yields on 10-year Treasury bonds.

These dollars also found their way into the U.S. stock market helping prop up stock prices.

However, as our relationships with allies become less certain and international trade policies create instability, this privileged position is beginning to weaken.

Foreign investors are becoming more hesitant to invest in U.S. stocks and bonds.

We saw evidence of this immediately after the tariffs were announced on “Liberation Day”, when long-term yields spiked as foreign holders of US Treasury bonds decided to sell first and ask questions later.

We also saw a sharp drop in the prices of U.S. stocks as international investors started to trim their exposure.

For the past decade, global investors and pension funds from Europe, Asia and Australia have all been buyers of U.S. stocks. As a result U.S. stocks trade at much higher multiples than their counterparts in other developed countries. Investors pay 50% more for each dollar of earnings for U.S. stocks than we do for similar non-U.S. stocks. This premium for American exceptionalism was based on 75 years of economic and political stability. However, this perception of stability among international investors is now fading.

U.S. retail investors have stepped in to buy the dip, which has driven a significant recovery in stock prices.

So while not immediately alarming, this trend poses meaningful long-term risks to our portfolios if left unaddressed.

The Potential Impact on Your Investments

If foreign investment in U.S. assets continues to decline, we can expect:

- Weaker Dollar: As investors move away from U.S. dollar assets, imports will become more expensive, further driving inflation

- Higher Inflation: Less demand for U.S. debt will likely lead to higher interest rates and coupled with increased inflation, reduce purchasing power over time

- Reduced U.S. Market Performance: Lower capital inflows may limit economic growth and lead to underperformance of U.S. markets compared to international alternatives

Recession risks are also increasing.

The lack of clarity around the trade and tariff policies is preventing businesses from being able to forecast their inventory, spending or hiring needs.

American Airlines just announced their earnings, and they provided 2 projections for the rest of the year. One in case of a recession, and another without a recession. We are going to see many more companies offer similar projections because they have no visibility.

Unlike larger businesses, with massive teams of analysts, small businesses do not have the man power to project multiple scenarios, nor do they have the liquidity or credit lines to survive extended periods of uncertainty. There are over 30 million small businesses in the US who will feel the pain of tariffs, higher interest rates and an economic slowdown. They will be more affected by a recession than the larger companies.

If we do enter a recession, we are likely to see considerably more volatility in the stock market for the remainder of the year.

Our Recommended Strategy Adjustments

To protect and grow your wealth in this evolving environment, we have:

- Increased cash allocations: In the short-term, we have been raising cash every time the market rallies. This will be reallocated to short-term treasuries, private credit funds and other global investments.

- Increased Global Investments: We’re strategically adding more international developed and emerging market assets to your portfolio. These regions offer strong growth opportunities, appealing valuations, and valuable diversification.

- Moderately Reduced U.S. Equity Exposure: We’re carefully decreasing your allocation to U.S. stocks. We still maintain significant U.S. market exposure, but at a more balanced level given the changing global landscape. We have also increased allocation to a private infrastructure fund, a thematic investment which is also expected to have lower volatility than the overall market, and a long-short equity fund as well. The risk of recession is severely heightened this year and a long-short fund will act as a hedge without sacrificing our exposure to U.S. stocks in case we are wrong.

- Maintain a short maturity of our bond holdings: We have been avoiding long-term bonds since the beginning of 2022. Most of our bonds have a maturity of under 5 years. This will prevent losses if long-term interest rates rise. We are also allocating to private credit funds, with maturity under 3 years but higher yields in the 8-10% range

- Tax Loss Harvesting opportunities: We will continue to actively seek tax loss harvesting opportunities to potentially lower your annual tax liability. This involves strategically realizing investment losses without altering your current asset allocation. By offsetting taxable capital gains, this process aims to improve your overall tax efficiency.

This strategy shift is not a reaction to short-term market movements but rather a thoughtful response to structural changes in the global economy. Our fundamental goal remains unchanged: to protect and grow your wealth over the long term.

Next Steps

If you have any questions about these changes and how they specifically affect your portfolio please don’t hesitate to reach out to discuss your individual situation. I’m committed to helping you navigate these changing economic conditions with confidence.

As always, keep calm and invest,

Nirav Desai

Risk Discloures: This is general information is not to be considered investment advice. Any investment included in this email whether, stocks, bonds, alternative assets, cryptocurrencies or commodities may not be suitable for all investors. Please consider your risk tolerance and talk to your advisor before making any decisions based on this email.