2022 was a year for the record books.

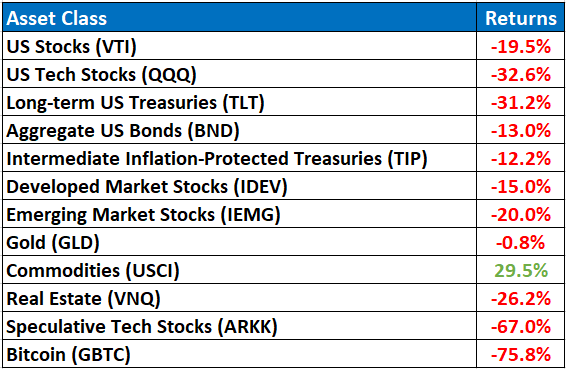

From an investment standpoint, it was pretty bad. Almost every asset class was down, and most of them were down double digits.

We saw the Russian invasion of Ukraine leading to the complete removal of Russian stocks from Emerging Market Stock Indices.

The UK bond market came unhinged and had to be bailed out by the Bank of England after threatening to create massive defaults in British pensions.

The Pound and the Euro saw the sharpest declines against the US Dollar ever.

US treasuries, which are usually considered safe havens during market declines weren’t spared either, as the fastest rate hikes in history raised interest rates from near zero in January to about 4% before the end of the year.

Mortgage rates doubled from 3.5% at the beginning of the year to nearly 7% at the end. The real estate housing market is frozen for now, but prices are softening across the board.

After decades of absence, inflation finally popped up and proved anything but transitory. The much-hyped Treasury Inflation-Protected Bonds (TIPs) didn’t provide as much of an inflation hedge as expected and were still down, although they performed slightly better than equivalent Treasuries.

The only positive asset class was commodities, being up about 30% as a group. In the face of the strengthening US Dollar, this outperformance is quite remarkable.

But even Gold, considered the ultimate safe haven, was about flat for the year.

And we saw the collapse of cryptocurrencies and the speculative tech trade.

Here are the returns for the most common asset classes, and their accompanying ticker symbol:

The worst performers were Speculative Tech stocks and Bitcoin, both of which were crushed in 2022 after seeing eye-popping triple-digit returns in 2020 (150% and 290% respectively).

High-flying stocks of yesteryear such as Tesla, Peloton, Rivian, NVIDIA, Netflix, and Zoom Video Communications all got crushed as their astronomical valuations finally caught up with them.

The more overvalued a stock was, the larger the losses.

That’s one inescapable fact of investing. Prices need to match valuations. When you ignore valuations and chase price performance, it eventually ends in tears and large losses.

Luckily, my portfolios are designed with value in mind. My clients and I weathered the storm with average losses between 12% and 15%.

Hedging our sensitivity to interest rates, and overweighting high-quality stocks with real earnings and cash flow helped prevent major losses. Exposure to commodities and gold helped offset our losses from real estate investment trusts. And further hedges helped buffer some of the losses in foreign markets.

Losing money is always painful, but all in all, it wasn’t as bad as it could have been.

And remember, the math of returns is geometric.

The more you lose in a bear market, the harder it is to catch up to breakeven.

It’s much easier to make 10% a year than it is 50%. The more you lose, the more risk you need to take in order to get back to breakeven.

Unfortunately taking more risk doesn’t guarantee a higher return – just a higher variance in the outcome. While you might make more money, you could also lose more money. This became painfully apparent to all the spec-tech & Bitcoin traders of the past few years.

This is why I prefer clients go through the financial planning process before we actually invest their money. Once you understand how much money you actually need to achieve all your goals in life, and we’ve qualified and quantified those goals, we should take the least amount of risk needed.

Yes, risk and return go hand in hand. There is no return without risk.

But the nature of risk is such that sometimes the return doesn’t show up when we need it. So, one should always focus on the potential risks, and not the potential returns.

Managing risk is much easier than managing returns.

Going into 2023, calls for a recession are rampant. Anytime I turn on CNBC, someone is calling for a recession. 2/3rds of surveyed economists predict a recession this year.

If this comes true, it will be the most widely expected recession in the history of mankind!

If you think everyone is extremely pessimistic on TV, you’re better off tuning them out.

Excessive pessimism makes you sound intelligent and making outlandish claims gets you more airtime on TV. After a while, no one remembers your claims so there’s no one to hold you accountable. But you do get a lot of free publicity, which leads to more recognition and interviews, and this eventually leads to more clients and more money.

But if you’re always pessimistic, your returns will be lackluster.

Personally, I think recession fears are overblown.

Despite all the talking heads on CNBC who keep shouting that the Federal Reserve will trigger a recession with too many rate hikes, and a recession is mandatory to curb inflation, I think the underlying economy has shown it’s quite resilient and a recession is not guaranteed.

Any recession we might see could likely be short-lived and mild.

That being said, I think inflation is likely to stay higher than the targeted 2%. Probably closer to the 3-4% range for the next decade. That’s a bigger concern to me than a mild recession.

There are 3 major inputs in inflation calculation: goods, housing, and services (or labor).

The prior 30 years saw peak globalization, with just-in-time inventory and cheap overseas labor putting a lid on inflation in the cost of goods. A strong dollar also helped with this, especially in the last decade. These trends are reversing, and the current focus is on reshoring or bringing manufacturing back to the US, resulting in higher costs.

There is currently a massive shortage of housing across the US. With interest rates at 7%, affordability has tanked and resulted in a sharp decline in home sales. This will likely trigger a recession in the housing sector. But the lack of supply will provide a floor under this, unlike the 2008 recession where supply far-exceeded demand. Once interest rates stabilize later this year, it’s likely mortgage rates will come down to a more manageable 5%, and home building and sales will pick up again. But the sub-3% rates are gone for good, so expect a resetting of home prices at some point in the near future.

The cost of services is driven by wages, and they’ve seen a sharp rise in the past year. Especially at the lower levels of society. While tech companies are announcing layoffs at the corporate level, many blue-collar jobs are seeing a shortage of workers and commanding top dollar.

I recently paid an electrician $100/hour for work around the house. He was the 5th person I’ve tried to hire. The previous 4 either never showed up, or ghosted me after the initial contact. Tradesmen are busy and have more work than they can handle.

Why is inflation a bigger concern than a mild recession?

If inflation is 4% over the next 10 years, the value of your savings drops 34%. Based on the past 20 years of historical data, where inflation ranged under 2%, the value of your savings only dropped 18%. A lot of online models still use this low 2%, which means there will be a shortfall retirement savings.

On the flipside, a mild recession is likely to be short-lived and have less of a financial impact.

Despite the chance of recession and higher inflation, I will be lightening up on my hedges this year. There’s no free lunch in investing. Hedging comes at a cost. When you hedge excessively, you pay a heavy price in the form of lower returns over the long term.

Lower returns are the price you pay when you hedge against volatility.

If you can’t accept volatility, then you must accept lower returns.

Otherwise, you can lower your risk by buying undervalued assets and avoiding overvalued or speculative assets.

After a decade of underperformance, I think foreign stocks will finally start to outperform US stocks. They are at historically and relatively low valuations and provide excellent entry points.

Bonds are also finally seeing a relatively high yield and are no longer a “returnless risk” asset.

Regardless of whether this year sees a continuation of 2022 or a rebound in asset prices, remember price is what you pay, value is what you get. If your investment horizon is long, and you are still in the accumulation phase, you will want stock prices to be cheap for as long as possible.

I wish you all a very happy and prosperous new year!

And, as always, keep calm and stay invested.

Regards,

Nirav