Hope you’re all ready to unwind and have some fun planned for the Memorial Day Weekend.

Not to throw a wet blanket on your fun plans, but I did want to bring to your attention some factors that are going to impact your future tax liability.

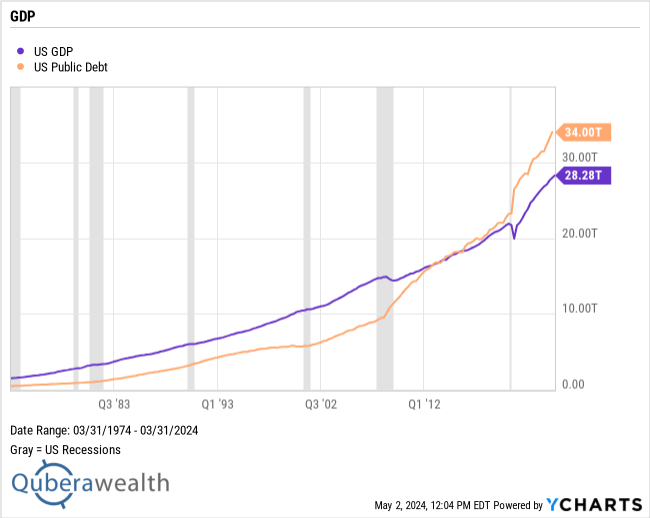

Rising National Debt

For decades the national debt was less than the GDP and both were growing at a similar pace.

Since 2010, the national debt has grown at a much faster rate than the GDP. It reached 100% of GDP in 2019 and has started to grow exponentially since Covid.

This rate of growth is unsustainable.

And government expenditures are not expected to slow anytime soon.

Taxes will need to be raised to bring down some of this debt. (Unless we let inflation erode the value of this debt, something the Federal Reserve is fighting hard against).

Over the long term, the trajectory for tax rates is higher. It might not happen overnight, but higher taxes are coming. I believe they will stay higher for longer.

This will happen regardless of who gets elected.

And in the near time, taxes are already set to go up. Even if Congress does nothing. (Or especially since Congress isn’t likely to do anything).

Tax Cuts and Jobs Act (TCJA) Sunsetting

The Tax Cuts and Jobs Act of 2017 included provisions with temporary tax relief. Many of these individual income tax benefits are set to expire in December 2025. This will result in higher tax bills for most taxpayers. For those in the highest tax bracket, the top rate will go from 37% back to 39.6%.

Estate Tax Limits Sunsetting

Under the TCJA, the current estate tax limit was doubled. Currently estates under $13.6m for individuals, or $27.2m for couples are not subject to the estate tax, which can easily get to 40%.

This higher limit is set to expire at the end of 2025 and the limits are going to get cut in half.

It’s expected these limits will go down to $7m for individuals and $14m for couples.

While this is more than enough for most people, if you already own $10m in assets and expect to live another 20 years, or own $5m and expect to live another 30 years, there is a good chance your estate will have to pay a 40% tax on part of your assets.

It’s the government’s last chance to get one more bite of the apple.

Net Investment Income Tax(NIIT)

For married households who file jointly and make over $250,000 a year, there is an additional 3.8% NIIT on interest income, dividends, capital gains, real estate and other passive income, royalties and non-qualified annuity income.

For married filing single filers, and single filers, it kicks in at a lower level. $125,000 and $200,000 respectively.

This is not indexed for inflation and will start to ensnare more and more people. A sneaky tax hike that no one pays attention to.

California Tax Increases

For those of you lucky enough to live in California, the disability insurance tax (part of payroll tax) of 1.1% used to be limited to the first $158,000 of income. As of 2024, the cap expired quietly. All wage income will now be taxed.

California also levies a 1% mental health services tax on income exceeding $1 million.

This brings the top rate in California to 14.4%.

If you’re in a high tax bracket, your top bracket (federal + state) is now 51.4%.

That’s what you’ll pay on short term capital gains too. For the past year, we were all excited about the 5% we were earning in Money Market accounts. Now we find the after-tax returns are under 3%. 🙄

Long term capital gains are taxed at a lower rate, but you’ll still pay up to 38.2%.

Luckily, there is no estate tax in California. 🤯

And social security benefits aren’t taxed either.

What You Can Do:

If you’re a high-tax earner, or have large one-time capital gains from sale of a highly appreciated asset, there are few ways to mitigate some of the tax bite.

If your estate is likely to be higher than the estate tax limits, there are some strategies we can look at as well.

The first step is to analyze your current tax situation and see where you are.

Schedule a Consultation: We’ll discuss your individual circumstances and explore potential tax-saving strategies.

I’ll also send you a link to upload your tax return directly into my tax analysis software. This will generate a tax report that will give us a basis from which to work from, optimizing the value of any tax deductions or credits and giving you a sense of how much you could potentially save through tax planning strategies.

By planning ahead, we can minimize the impact of potential tax increases and ensure you are utilizing all available tax-saving opportunities.

I will continue to monitor tax policy developments and keep you informed of any significant changes. In the meantime, please don’t hesitate to reach out if you have any questions or concerns.

Sincerely,

Nirav